A 28-year-old nurse in Denver who maxes out her 401(k) every year will retire with roughly $900,000 after 35 years of diligent saving. Her colleague earning the same salary, but able to safely finance five times larger contributions, will retire with over $2.3 million. That $1.4 million gap isn’t about financial literacy or discipline, it’s about access to capital.

This is America’s ownership crisis in microcosm. Forty percent of Americans own no financial assets whatsoever, not because they don’t want ownership, but because they’ve been systematically locked out by timing and capital constraints. Basic Capital exists to eliminate that barrier.

A New Kind of AccessBasic Capital’s ambition is audacious. The company aims to become the financial infrastructure that democratizes wealth-building at scale. They’re not just building a retirement product, they’re laying the foundational rails to close America’s ownership gap, starting with the $35 trillion retirement market but designed to extend far beyond it.

They’ve built what is essentially a “mortgage for retirement”—a financing structure that lets people contribute up to five times more to their retirement accounts, without personal liability or margin risk. This is not speculative trading. It’s structured financing, vetted by retirement and securities lawyers, and invested in diversified portfolios built for long-term compounding. For users, the experience is elegantly simple. Underneath, it’s a sophisticated orchestration layer connecting payroll systems, retirement custody, regulatory compliance, and institutional capital markets.

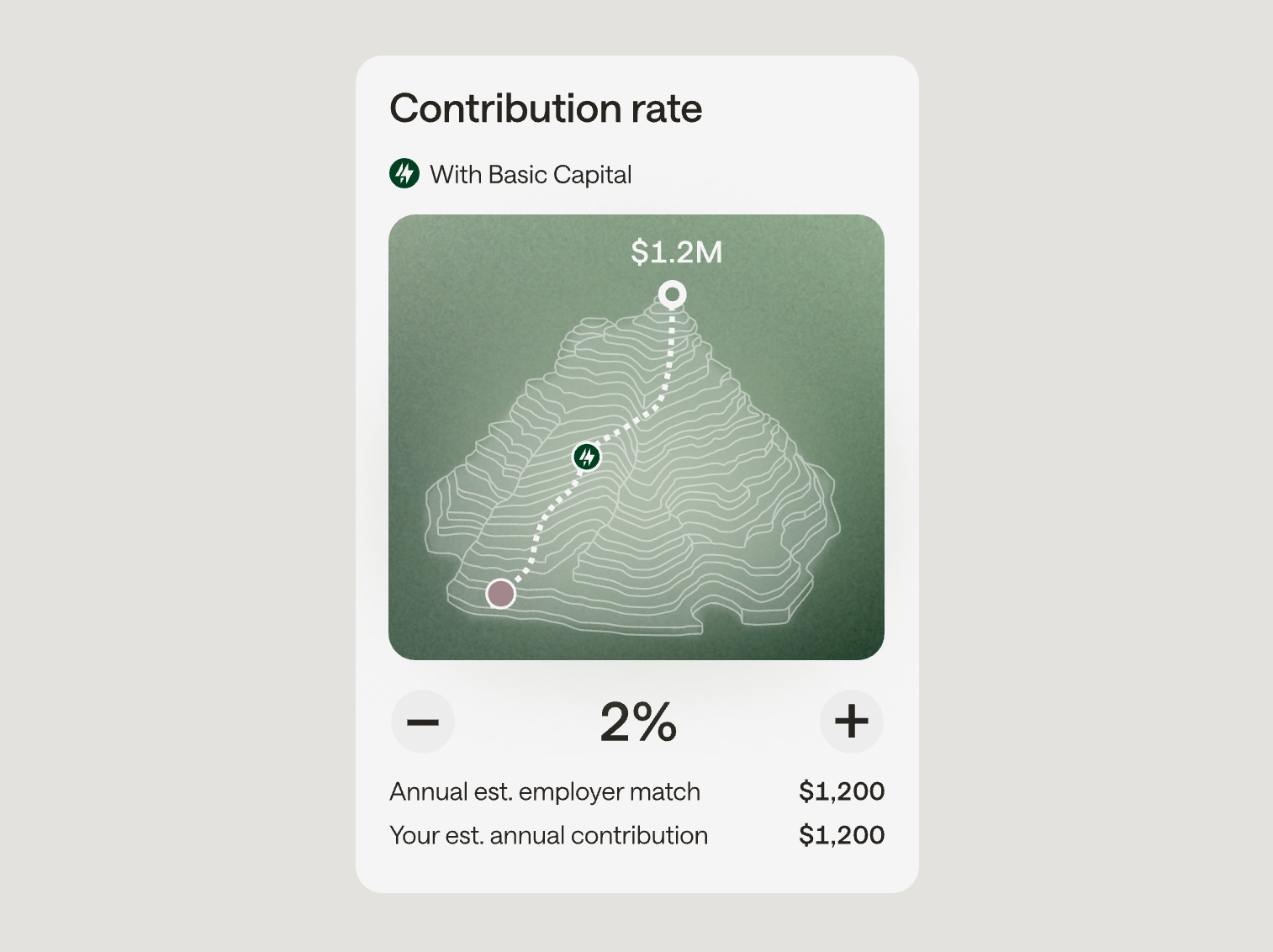

“A small shift in access to capital can mean the difference between anxiety and security.”Consider Maria, a 35-year-old teacher who earns $55,000 and can barely afford to contribute $200 monthly to her retirement. Through Basic’s financing, she can effectively contribute $1,000 monthly while maintaining the same cash flow. Over 30 years, that transforms a $240,000 retirement nest egg into over $1.2 million, the difference between financial strain and true stability. Or think about the 26-year-old software engineer who knows compounding works best when you start early but is paying off student loans. Basic gives her the power to act immediately, borrowing against future gains the way homeowners build equity over time.

The Moment Has ArrivedThe bottom half of American households own less than one percent of equities, not because they don’t want ownership, but because they’ve been locked out by timing and capital constraints. Basic Capital changes that equation fundamentally.

The moment for this change has arrived. A perfect storm of cultural, behavioral, and regulatory shifts is making Basic Capital’s model possible. Wealth inequality has reached levels not seen since the 1920s, and younger generations increasingly view traditional wealth-building timelines as inadequate for their reality. They’re not afraid of leverage, they’re afraid of missing out on wealth creation while they wait decades to catch up.

“They’re not afraid of leverage, they’re afraid of missing out on wealth creation.”Early traction shows this is more than theory. Over 90 percent of users opt into financing when offered. This isn’t reckless speculation—it’s calculated empowerment by financially literate professionals who understand that productive leverage, properly structured, is how wealth gets built.

Traction You Can MeasureMarket and regulatory conditions have aligned. President Trump’s recent executive order “Democratizing Access to Alternative Assets for 401(k) Investors” recognizes that “more than 90 million Americans participate in employer-sponsored defined-contribution plans, yet the vast majority of these investors do not have the opportunity to participate in the potential growth and diversification opportunities associated with alternative asset investments.” The administration is actively working to remove barriers that have denied Americans access to the same investment opportunities available to the wealthy and to institutions. This regulatory tailwind, combined with capital markets opening to retail investors, private credit yielding attractive spreads, and fintech infrastructure maturing to support complex flows at scale, creates an unprecedented moment for Basic’s approach. What would have been prohibitively complex to build and maintain just a few years ago is now technically feasible at scale.

The results speak for themselves. In just months, Basic has onboarded 12 employers across sectors from healthcare to technology, welcomed over 800 active users, and built a waitlist exceeding 5,000. That 90 percent-plus financing opt-in rate isn’t just impressive, it’s proof of product-market fit for a fundamentally new category. The business model is diversified across admin fees, asset-based fees, and financing spreads, with a clear path to profitability within 30 months.

The Team to Build ItThis team was built for the challenge. Founder and CEO Abdul Al-Asaad’s life story reads like the mission statement itself—from a Syrian refugee camp to Goldman Sachs’ distressed credit desk, where he structured complex financial instruments, to Harvard Business School as an Arthur Rock Scholar. His journey from displacement to the pinnacle of American finance embodies the pathways to wealth that Basic aims to democratize. He’s surrounded by seasoned operators from Stripe, Uber, Robinhood, and Square—engineers and designers who’ve scaled regulated consumer finance platforms and understand that building trust requires both regulatory rigor and elegant user experience.

At Forerunner, we invest in companies that create structural behavioral change in how people live, work, and build wealth. Basic Capital represents exactly that transformation. They’re starting with retirement savings, but their infrastructure is designed to extend across the full spectrum of personal wealth-building. We see a future where Basic becomes the foundational layer connecting individuals to capital opportunities, transforming how Americans build wealth over their lifetimes.

A Future Without Timing LimitsThis is a bet on a future where the accident of timing—when you start earning, when you can afford to save—doesn’t determine your financial destiny. It’s a vision where the single mother working two jobs can build generational wealth alongside the investment banker. Where your twenties become the decade you accelerate toward financial freedom, not the decade you struggle to get by.

“The wealthy have always used leverage to build wealth faster. Basic Capital is democratizing that advantage.”And we couldn’t be more excited to help them rewrite the rules of American wealth-building.